Whole Life Insurance Introduction?

Whole Life Insurance is a kind of permanent insurance plan that offers insurance protection to the customer throughout the insured persons above a certain age provided the premiums are paid. While it is possible to compare term life insurance which provides coverage to the customer for an agreed period with whole life insurance, the latter means the company will pay the death benefit to the beneficiaries whenever the insured passes on.

Whole life insurance has one of the special components, and it is the cash value component. An element of every premium that is paid goes to the cash value and gains interest, or dividends, over time. This cash value can be borrowed in form of loans or be fully withdrawn wherein will serve as a source of funds during the policyholder’s life time.

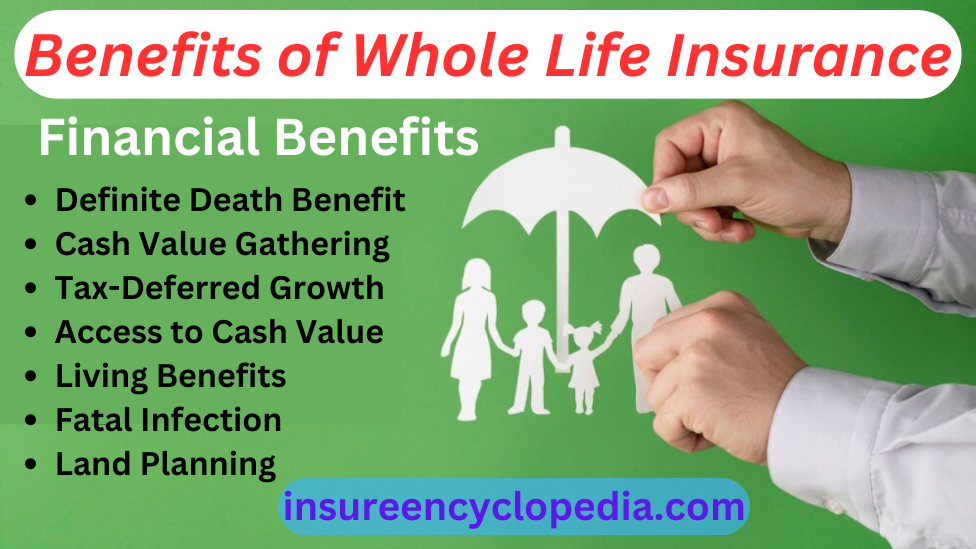

Benefits of Whole Life Insurance:

Financial Benefits

- Definite Death Benefit: Pays a specified sum to the beneficiaries on the death of the insured where it may happen later.

- Cash Value Gathering: Out of the premium, some is paid to cash value and on this, for policyholders, has a compounding on the tax preferred basis.

- Tax-Deferred Growth: The component known as cash value is preferred on the premise that it is invested and it grows tax free hence has the potential to grow at a faster rate than the other accounts that attract tax.

- Access to Cash Value: It permits policy loan against or withdrawal from the cash value under certain circumstances which can be considered as safety net.

- Living Benefits: Some riders are offered to other Riders, and these include; But many policyholders prefer the following accelerated death benefits:

- Fatal Infection: In scenarios where the coverage’s client is diagnosed with fatal infection, then the coverage pays immediate full amount to the client.

- Land Planning: Can help in avoiding estate taxes on an estate and provide cash to the beneficiaries.

Non-Financial Benefits

- Peace of Mind: Most of your family members and close friends will find a lot solace and comfort when they are informed that they will be well off should you die unexpectedly.

- Legacy Building: Whole life insurance is therefore useful any time that you want to make a bequest for your family.

- Guaranteed Premiums: Whole life insurance policy is different from the term insurance policy in terms that the premium to be paid in whole life insurance policy remains the same throughout the policy period.

Therefore, it is always advisable to always have in mind the financial goals that you possess or the financial needs that you might in future need to attend to as you make your choices.

Whole Life Insurance Costs:

Whole life insurance costs more than term life insurance because of the cash value component apart from it being a life time policy for the holder. However, the exact cost varies significantly based on several factors: However, the cost is not fixed in that it varies with other several factors as explained below.

The following factors are known to affect the cost of the policy

- Age: This has been echoed time without number that new generation policy holders are likely to be presented with lower premium rates than those of the older policy holders.

- Health: As would be expected, good health of the clients could be taken as implying that only a low premium to pay.

- Coverage Amount: The premium depends on the part of the death benefit the higher the part the higher the premium.

- Policy Type: Also, different whole life policies themselves have rather different fee arrangements.

- Insurer: The insurance companies have different insurance rates and the insurance policy may or may not have the following features.

Family Life Assurance Policy:

Whole life insurance it is one of those financial products which should assist in attaining the financial potential of the family. It offers them insurance cover to their family and also serves an investment corridor ideal to most families.

How Whole Life Insurance protects your family?

- Guaranteed Death Benefit: Ads to your family an economic power that will enable it to be fed in the event you die unexpectedly. It can be in used to cater for funeral expenses, house and other utilities, tuition fees and other basic needs among others.

- Cash Value Accumulation: As a result, the premium is only partly reflected and your policy is expected to provide you immediate money for life emergencies or college education of your children.

- Estate Planning: Whole life insurance can be incorporated in an estate plan and it will help in passing down of an estate to the next generation.

Whole Life as Element of Estate Planning:

As it has been mentioned, whole life insurance is one of the most effective methods for estate planning. It can assist with the ability to pass on assets seamlessly, as well as offer the beneficiaries’ financial stability.

How Whole Life Insurance can assist your lands?

- Liquidity: Definitely one of the biggest challenges of estate planning is to generate adequate working capital to realist estate taxes, debts and cost. Whole life insurance can make a huge estate tax liquidity payment at the death of the insured helpful in maintaining the current business assets intact.

- Estate Tax Coverage: Where there will be federal estate taxes, whole life insurance becomes useful for paying this amount so the legacy left behind for the heirs is the largest one possible.

- Business Succession: In the case of the business owners, whole life insurance should be used for paying estate taxes, for the business valuation as well as such matters as the buy-sell agreements that facilitate the transfer of the business empire.

Summary of Whole Life Insurance:

Permanent life insurance is a plan in which the policyholder gets coverage for the whole life, and whole life insurance is one of the permanent. It has a cash value which one may borrow money against, and it pays a death benefit to the beneficiaries at the death of the policyholder.

Term insurance, on the other hand, is pure, with practically no cash value to talk about; whole life, however, builds cash value over the years which may be borrowed against or even surrendered. Benefits too are also another non- linear determinant because they do not alter throughout the life time of the policy. Whole life insurance costs more than term life by a small margin, however, in estate planning, it is one of the most valuable asset and offers future opportunities for the enhancement of the future gain.

Get more Information About Insurance: