What is Product Liability Insurance?

Product Liability Insurance is an insurance policy which offers insurance for product liability losses occasioned by faulty goods. Product liability insurance is a business insurance policy that can guard your enterprise against financial loss in the occurrence that a product you produce, offer, or sell result in harm or damage to another person.

In simple terms, it is a cushion against legal cases and compensation demands for manufactured products’ damage. This insurance contains legal expenses, claims for personal injury and property damage.

Types of Product Liability Claims:

- Manufacturing defects: Produce failure resulting from mistakes in fabrication, assembly, testing etc.

- Design defects: Faults that are inherent with the product, leading to the harm of people.

- Marketing defects: Pre-sell communications where the information about the product is wrong or intended to deceive.

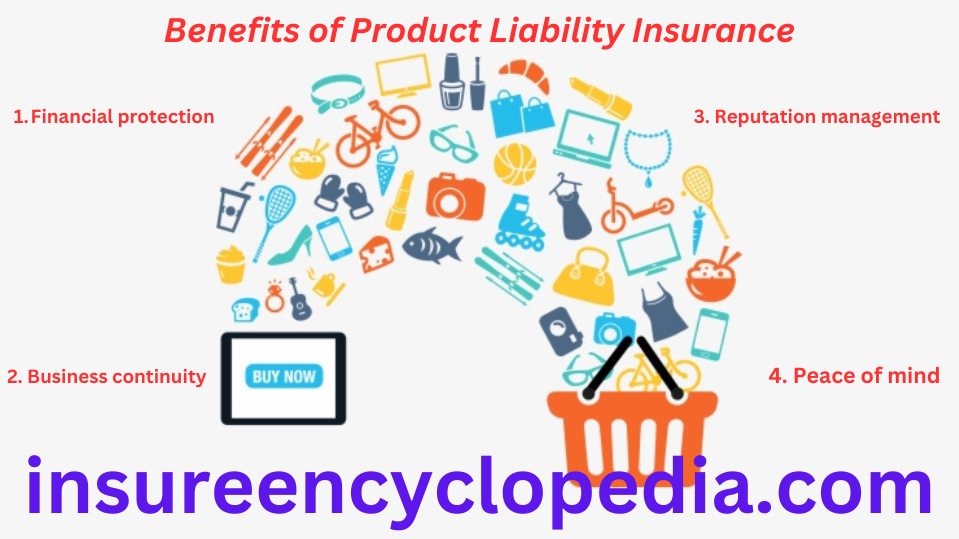

Benefits of Product Liability Insurance:

- Financial protection: It pays legal costs including fees for lawyers and other representatives, settlements and different kinds of judgements.

- Business continuity: Assists in continuity of business in the event of a product liability claim.

- Reputation management: Safeguards your brand reputation.

- Peace of mind: Assures the organization on its business transaction and processes.

How Product Liability Insurance Works?

A product liability insurance is a sort of insurance policy that offers protection to a business in the event of the injuries and or damages of products manufactured.

- Policy Purchase: Business acquire product liability insurance from insurance firms.

- Incident Occurrence: When a business distributes a product that results in harm of a person or damage of property then there is a claim submitted against the business.

- Insurance Coverage: After the incident occurs the insurance company looks at the claim made regarding the policy and evaluates if it is valid according to the policy or not.

- Legal Defense: Where the said claim is true and recognized, the insurer is legally expected to give legal representation and any expenses in the same process.

- Financial Compensation: If the business is determined to be at fault the insurance company, then pays for the costs of the damages, settlements or judgements as per the limit of the policy.

Key elements of product liability insurance:

- Coverage for injuries: Doctors’ fees, lost income, and suffering.

- Coverage for property damage: Expenditure incurred in compensation for properties that have been affected in the disaster.

- Legal defense costs: First of all, pays for legal services of attorneys and other expenses such as court fees.

- Product recall expenses: May include cost of some product recalls depending on organizational circumstances.

This will help businesses to know how the product liability insurance works so as to safeguard their future from financial loses in the off chance that a product related claim came up.

Who Needs Product Liability Insurance?

A product liability insurance ought to be taken up by any company that is involved in the manufacturing supplying or selling of a product.

- Manufacturers: The companies, which physical produce the deliverable tangible goods or services that can be shipped through a channel of distribution.

- Retailers: Sellers, regardless of whether or not they themselves manufacture the merchandise in question.

- Wholesalers and Distributors: A list of some of the actors in the supply chain.

- E-commerce Businesses: Those merchants that engage in offering tangible Products over the internet.

- Food and Beverage Companies: Those categories that include the business that deals with manufacture or sales of foods and beverages.

In other words, if your business is in the circulation of physical products then you should consider taking Product Recall Insurance. The coverage is generally global to service industries where those industries rely on the products for delivery of their service.

Claiming Product Liability Insurance:

- Immediate Notification: As soon as you get an insight of a potential product liability claim, notify your insurance company.

- Gather Evidence: I also make sure I obtain all the documents that we availed or which were taken by the EMTs, the witnesses, the police and any other document from the product details, to the details of the incident to the medical and picture.

- Legal Representation: Always consult the lawyer to learn what you are legally accorded and the things that should be done.

- Claim Filing: Such an importance is attached to ensuring that as much as one can describe the circumstances under which the incident occurred in the claim form for the insurance company.

- Investigation: In insurance business, the insurance company will wish to know whether or not the claim will be paid hence undertake the claims adjustment.

- Defense: If the claim is valid the insurance will provide a legal counsel that will defend the business.

- Settlement or Judgment: The claim can be resolve without going to the court or the claim can be resolved legally.

Important Considerations:

- Policy Review: The fine details of a particular policy, including its policy limits and exclusions, is best to have basic understanding on.

- Quick Action: In case of occurrence of such mishap, one is required to give notice to the insurance company at the earliest opportunity.

- Cooperation: Make sure you will passionately work together with your insurance company and also your hired legal lawyer.

- Documentation: The notes taken during investigations; Every note that has been taken with respect to the claim; All forms of communication should be documented.

- Risk Management: May be adopt such measures that a manufacturer would not want to have a product liability claim against him/her.

Conclusion:

Product liability Insurance is considered to be one of the policies used in risk management in organizations that involve in manufacturing, selling, and supplying of products. It works as an insurance against probable litigation resulting from injuries or loses as a result of using the specific product. When firms tender their products in liability insurance, they get the guarantee of the financier’s comfort and reliability in addition to ensuring continuity of their business in the event of occurrence of challenging risks and losses.

Since product liability claim is always higher in cost than other uncertain events, insurance may be look like as an additional cost to those in the process of producing a product. An insurance agent has to be approached to come up with the figure to be insured depending on the level of vulnerability of the business. Another concept that careers should know in eliminating product liability claims is risk management and that is why it is significant that careers know that products possess risks in a bid to decrease the possibilities of such cases.