Introduction of Life Insurance?

Life Insurance is an agreement between the policyholder and the insurer or assurer where the insurer in return for an agreed premium guarantees the payment of a stated amount to the beneficiary upon the occurrence of the insured’s demise. Other circumstances that bring forth the payment include; other circumstances include situations whereby the contract makes provisions such as terminal illness or critical illness.

In other words Life Insurance is a form of an insurance policy that protects the beneficiaries in the event of your premature death. In return, you agree to contribute regular premiums which assure that they receive cash when you are no longer alive.

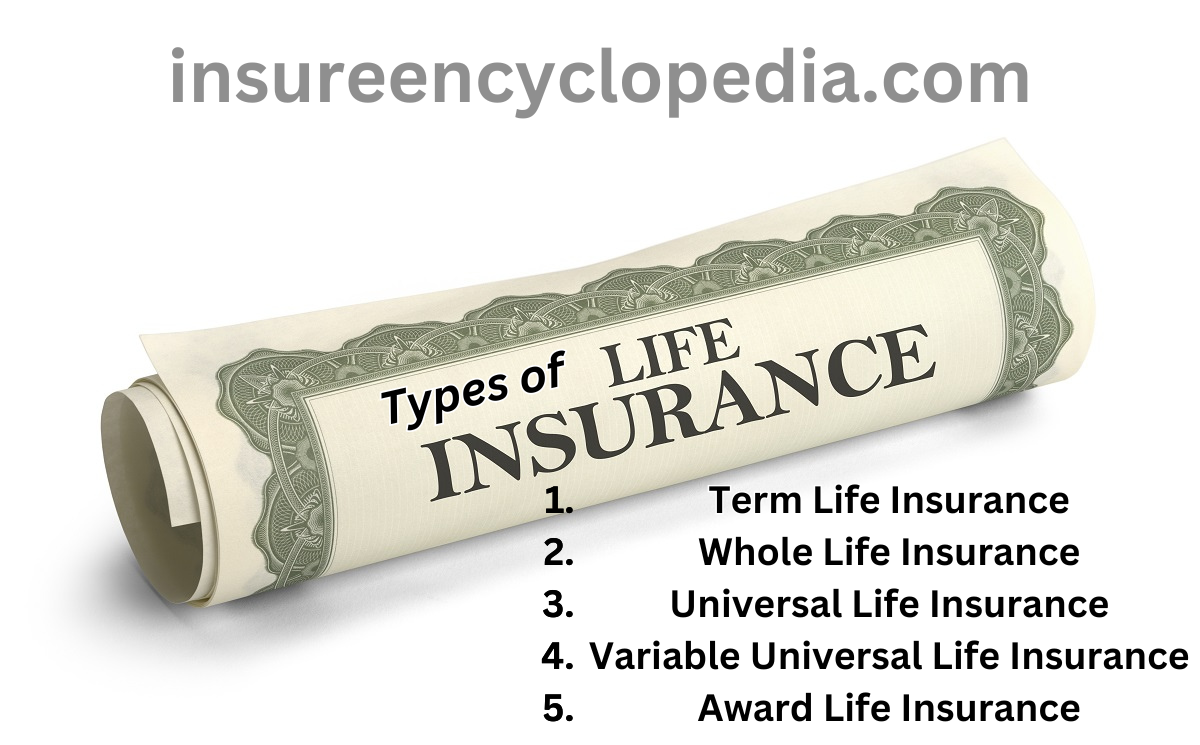

Types of Life Insurance:

There are number of products under life insurance and each and every kind of product is used to fulfill certain need of an individual hence the fund’s aim.

1. Term Life Insurance

- Coverage: Pays a face amount for a certain term and then, in return, paying a death benefit.

- Cash value: It does not even begin; no flush of cash value is ever accumulated.

- Best for: Individuals that have short-term insurance needs, for example, home mortgage, or users that at that time when a childbearing stage is realized.

- Whole Life Insurance

- Coverage: Comes with lifetime benefits when taken alongside the cash value that is paid to the policy holder when the death happens.

- Cash value: Builds up the value of cash over time, and can be replenished to provide cash in the form of a loan.

- Best for: The buyers of the conventional bought insurance, those people who wish to have insurance coverage for the future or, actually, for indefinite time, and also, people who would like to build up their wealth by investing in the insurance plans.

- Universal Life Insurance

- Coverage: Is comprehensive in its provision of benefits and can also have a cash value riders included on it.

- Cash value: Cash value growth has to do with the earn out of invested funds in a policy.

- Best for: Anyone who wishes to make an investment and at the same time take a life policy.

- Variable Universal Life Insurance

- Coverage: Universal life with options for investments predetermined and managed by the policy holder.

- Cash value: Their finding shows that performance of investment has a direct influence on the cash value growth.

- Best for: Those people who possess investment skills and those individuals that want to take risk.

- Award Life Insurance

- Coverage: It serves as a life insurance policy and at the same time as a savings plan.

- Cash value: Collects the value in cash all along the period of the policy and then pays a lump sum to the owner of the policy after expiry of the policy.

- Best for: The individuals who have long term savings and more appropriately for the insurance products where the policyholder pays the premium periodically and is repaid a lumpsum amount either on occurrence of death of the policyholder or any such event as described by the terms of the policy.

Term Life Insurance with Return of Premium:

- Coverage: on the occurrence of the insured event namely death when the policy term is still active pays out the face value and if the policy term expires and the insured is still alive then all the premiums are refunded.

- Best for: It is for those people who would want their families and loved ones to have financial security in the event of their demise, with a variable depending on the type being the return of the premiums paid.

How to Choose a Life Insurance Policy?

In all the vital as well as confidential financial decisions throughout their relationship, they are expected to choose the right life insurance policy.

Understand Your Options

- Research different types of life insurance: From these options, it is quite easy to get to know the term life insurance policy also commonly known and referred to as the whole, universal as well as the variable universal life insurance policy.

- Compare features and benefits: Assess it in terms of coverage, in terms of the speed of producing the amount that are available for cash, the premium and the other add-ons termed as the riders.

- Consider your risk tolerance: The thing that you should know about VUL or variable universal life insurance is, it should also prompt you to look at your capacity to handle risks in investment.

Assess Your Needs

- Determine your coverage needs: To determine the extent of coverage understand your dependents needs in order to determine the amount of cover the client requires they need to consider the following needs of their dependents.

- Identify your budget: Decide on the amount of dollar that can be spent in order to cater for pay of the premiums.

- Consider your long-term goals: Determine if one is a taking a life insurance policy to fulfill a need or with an expectation of getting value added.

Get Quotes

- Use online comparison tools: On falling on a conclusive list of prospective service providers one discovers that there are many firms which provide free life insurance quotes online.

- Consider discounts: All insurers allow customers to enjoy a discounted price and one ought to ask the insurers for discount rates such as for non-smoker clients, those who take multiple policies from the same insurer or those in the insurer’s company.

Review the Policy Carefully

- Understand the policy terms: In every Policy Section and all the documents connected with it, one has to realize what is permitted and what is prohibited, and if the former is the case, to which extent.

- Check the financial stability of the insurer: Besides, let’s try to get the quotations from the independent insurance agents, as far as insurance is concerned.

- Consider additional riders: They should decide whether to retain an optional coverage such as accidental death or dismemberment or long-term care.

Make an Informed Decision

- Consult with a financial advisor: It is probably wise for ones to consult on what the best action to take particularly from a certified financial planner.

- Review your policy regularly: It is always good to advisable to cross check if one still requires the coverage that is given by the policy at some time in his or her life.

- Remember: Selecting an appropriate life insurance policy is one that has to do with factors that are inherent in the client. This I must explain do not be in a hurry make comparisons and go for a policy that meet your needs and your pocket.