What is Home Construction Insurance?

Home Construction Insurance is a ‘limited sense’ property insurance which means that a policyholder can seek coverage during construction or reconstruction of a home. This one is designed to protect the building materials, fixtures and equipment used in the construction project against loss in a variety of causes like fire, theft, vandalism, natural disasters plus others.

Where homeowners insurance is for completed properties, Home Construction Insurance is created to fit construction risks involved in construction works. It offers contractual protection through all phases of construction and ensure that one does not financially strangulate by surprises along the process. Home Construction Insurance also play a vital role in our daily routine life.

Why is it Important?

- Protection against unforeseen events: The construction project is always associated with high risks and the possible risk could be natural disasters, accidents among others. In this context, one can state that home construction insurance is a solution that helps in reducing the loss under these conditions.

- Coverage for materials and equipment: It protects the construction material, facility, as well as equipment used in construction to mean that in the event that they are damaged or destroyed you will not have to use your own money to put them back.

- Peace of mind: Oh, how I would love to have a private insurance for those structures which are under construction and also for the human heart which stirs up along with those structures.

- Compliance with financing requirements: A large number of the lenders will request the homeowners to include home construction insurance for construction financing.

Protection for contractors: It can also protect the contractor against legal claims in a scenario where the contractor is also legally liable for loss of the property or death within the construction site.

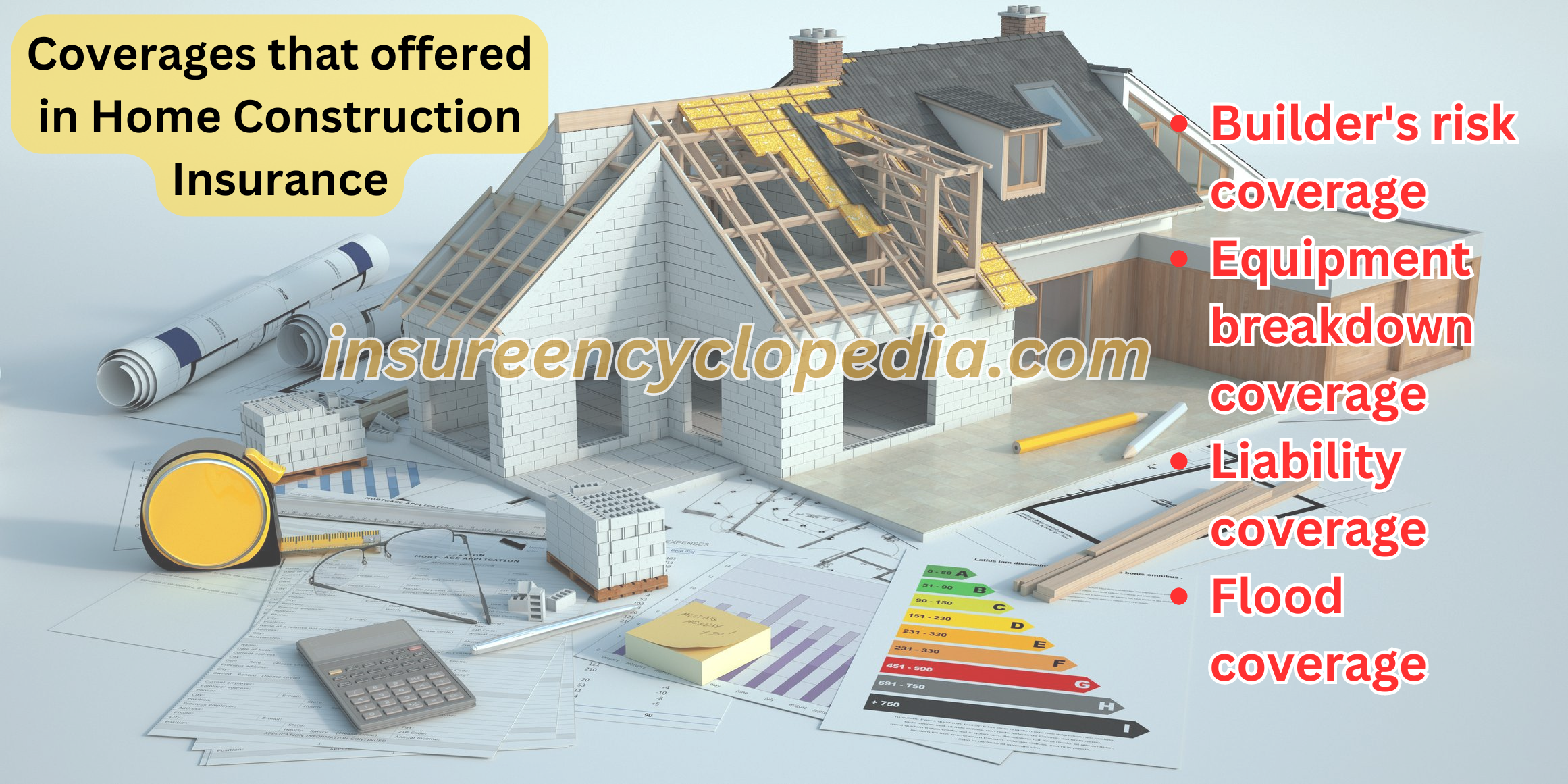

Coverage types that can be offered in Home Construction Insurance:

- Builder’s risk coverage: It is the simplest type of insurance contract that guarantees all the constructions materials, fittings and all the necessary equipment.

- Equipment breakdown coverage: This includes the losses on the construction tools, equipment like cranes, excavators and generators among others.

- Liability coverage: This provides the insured with adequate protection in as far as legal liability on emerging claims of bodily injury or property damage in relation to the construction undertaking is concerned.

- Flood coverage: This is an additional coverage by which one is covered for any loss in case of flood.

Home Construction Insurance generally covers:

Any form of negligible interference with the building’s material items, fittings and installations earlier employed in the construction phase.

- Damage caused to properties by fires, theft, acts of vandals, floods, hurricanes plus other disasters.

- Damage to construction equipment.

- Liability for contracting any form of harm on the people or the destruction of property due to the construction.

Home Construction Insurance may not cover:

- Vandalism and Arson or intentional act, in which an individual constitutes themselves to be a willful fire raiser in setting ablaze property of another.

- The company incurs cost as a result of the machines or the hardware getting old and gradually becoming less efficient.

- Fault which arises out of design, and accident that happen during construction or committed by the construction workers.

- Damage caused by shifting of the earth as in an earthquake or a landslide and the like.

You must always make sure that you go through your policy so that you have an understanding of what is provided when and what is not.

Benefits of Home Construction Insurance:

- Protection against unforeseen events: It is useful within a home construction project in the sense that may probably happen during construction hence the cost incurred for insurance is controlled.

- Coverage for materials and equipment: It ensures that you shall refrain from having to be billed for the next set of damaged materials or equipment’s.

- Peace of mind: This is because in the case of an occurrence of a loss, risk or damage on the construction project then the owner has the option of making a claim on the insurance policy.

- Compliance with financing requirements: Almost all the builders will require the borrower to obtain a home construction insurance before they are granted the construction loan.

- Protection for contractors: It can also shield contractors from a lawsuit for liability for property damage, or occurrence of an accident at construction sites.

Key Considerations for Home Construction Insurance:

- Coverage limits: Health insurance: discover how much each of these events your insurer will cover up to the hilt.

- Deductibles: Be aware of the extent to which you will incur the expenses which are not catered for by your insurance policy.

- Exclusions: In particular, be realistic and know that there is no situation east of the mentioned policy or policy might not cover some event or circumstance.

- Additional riders: Consider whether there is the need to obtain additional cover for certain perils regarding such as equipment breakdown or floods.

- Insurance company reputation: Firstly, it is suggested performing the analysis of the insurance company’s solvency status and customers’ satisfaction.

- Policy terms and conditions: One should look at the policy language as some policies have rather vague language in their statements; thus, it is crucial to read the policy language to determine the terms and conditions that belong to those policies.

Comparing Policies for Home Construction Insurance:

- Coverage limits: Council the maximum amount that can be claimed in respect of different kind of loss.

- Deductibles: Select the most preferable amount of the deductible that you can afford in case of an accident or any other situation.

- Premiums: In this approach, the price of several policies is determined with an aim of establishing the lowest price prevalence in the market.

- Exclusions: Look out for any significant variation in the policies that exclude and do not exclude certain diseases.

- Customer service: As well as take time and think about the sort of customer satisfaction the insurer has to offer and the pace at which these insurers are willing to attend to their customers.

- Additional riders: Figure out how many extra but indispensable riders can be, and compare the costs of getting them.