General Liability Insurance Introduction?

General Liability Insurance are, per chance, concerned with the legal and fiscal risk that are inherent in the operation of any business? You’re Business Safety Net liability insurance remains one of the insurance policies that every single existing company without exception should take. This protected you from legal liabilities which may warrant your arrest, or compel you to pay for violence, property damage or losses, or any other thing that may be associated with the operation of your business.

All in all, speaking about the given type of insurance, it is possible to state that it is rather effective and can help the company to prevent a financial failure in case of definite accidents or claims. To a person who has a small shop selling simple goods, it is as important to another with a large business corporation as is a general liability insurance in that it is insurance that helps a business avoid an undesirable occurrence.

Why General Liability Insurance is crucial to businesses?

- Protection against lawsuits: It is for bodily injury to third parties, property damage, and advertising injury.

- Financial protection: Includes the cost of lawyers, and damages awarded in and out of court.

- Business continuity: That physical and capital assets of the firm can carry on business without disruptions occasioned by losses from legal actions.

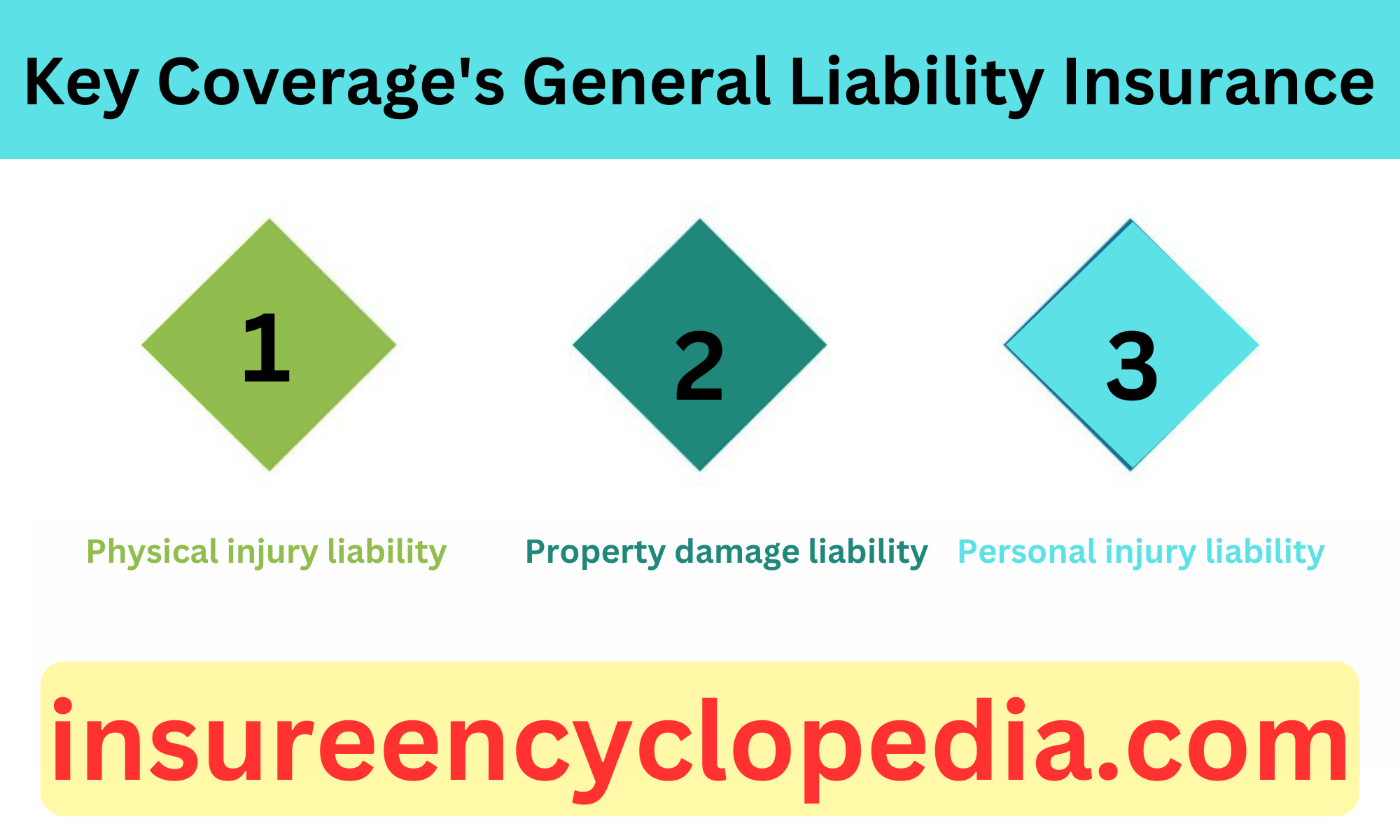

Key Coverage’s of General Liability Insurance:

- Physical injury liability: Exempts the policyholder from lawsuits for shock, medical bills, lost wages and other damages in case a client gets injured in the business owner’s property or from his business operations.

- Property damage liability: Pays when the business operations of your company result in the loss or damage of another party’s property.

- Personal injury liability: Safeguards the organization from prosecution under the law of copyright infringement and other forms of defamation.

Factors Affecting General Liability Insurance Cost:

Several factors influence the cost of general liability insurance: Several factors influence the cost of general liability insurance:

- Industry: Indeed, varied research indicate that higher-risk employment sectors, for instance construction or manufacturing, offer more.

- Business size: As the number of employees and the amount of revenue increases, costs might increase, therefore big businesses can incorporate high costs.

- Location: There might be in dependencies such as high crime indexes or natural disasters, which may result to higher premiums.

- Coverage limits: As to the amount of coverage, it determines the premium.

- Claims history: This is due to previous claims making car insurance rates higher or even cause car insurance refusal.

Advantages of General Liability Insurance:

- Financial Protection: Helps to provide protection from lawsuits, fines, penalties, legal fees, judgement and settlements which can potentially bankrupt a business.

- Peace of Mind: It is comforting to know that business owner can avoid a sudden lawsuit, then turn his or her attention to the business.

- Business Continuity: Assists to keep operations going in the event of a claim, so that costs are met.

- Customer Confidence: Shows that you are safety and responsible and therefore are trustworthy to the customers.

- Contractual Requirements: It is common to be asked for a proof that general liability insurance is in place for ongoing pregnancies.

- Asset Protection: Exempts your individual assets from risks that arise from business operations.

Disadvantages of General Liability Insurance:

- Cost: These differ with the nature of the business; size and geographical location among others and end up as other expenses to the business.

- Limited Coverage: It does not extend cover for all risk that may occur at the workplace for instance employee injury or own business damage.

- Claims Process: On the filing and processing of the claims, they could at time be stressful and time taking exercise.

- Increased Premiums: This simply means that through the claims the premium rates can be very high in future in case the insured is in need of the money.

- Policy Exclusions: So as to ensure that they do not form part of policy exclusions they have to be well understood so as to be avoided hence making the insurance capable of meeting all the aspects required.

General Liability Insurance Exclusions:

However, to understand the disadvantages of this service, it is important to know what general liability insurance does not protect against. In other circumstances, there are some things, the costs of which cannot even be partially insured.

Common Exclusions

- Employee injuries: The employees of emergency services are covered by the workers compensation insurance provision.

- Auto accidents: Must have a have commercial auto insurance.

- Professional services errors: Protected by Wall of Professionalism.

- Contractual liability: However, those categories are not listed in the domain of coverage under the basic policy, but are generally taken with an endorsement.

- Pollution: The costs of pollution and similarly other costs of loss are normally excluded from the calculations.

- Intentional acts: Suicide it does not include the intentional act which the individual performs with the intention of inflicting harm on himself/herself as well as on others.

Conclusions of General Liability Insurance:

The foregoing exclusions in General Liability Insurance demonstrate that every policy has the special characteristics of coverage and prohibition. This is an insurance that provides rather limited cover for most hazards of business and does not come close to address all the aspects of business liability. The study has revealed some of the following about them: Among the discoveries, it is clear that businesses will have to seek to find the gaps that these exclusions have left in coverage. In fact, professional liability, worker compensation, environmental liability, cube liability and use of internet are some of exposures that are not covered by general liability insurance.

Any Companies which enter into operation s in industries where such risks are inherent should also look at other special business risks insurance such as Professional liability, workers environment compensation and cube insurance. But, just as with limits of liability, exclusion for incidental acts, forum exclusions for intentional acts, and for damage to business owned property, prove that risk administration and legal consultation are a large concern within a business. There are excluded claims that business entities have to avoid and which contractual obligations are assumed by them in their transactions.