What is a Cyber Liability Insurance?

In the light of above discussion, cyber liability insurance can be explained as a tailored made policy that addresses risk management for any loss that emanates from cyber terrorism or a hacking incidence. That serves to prevent and minimize the expenses required to address these more frequent accidents.

In fact, it is an insurance especially for the modern world, in which it is particularly important. With the increase in reliance on Information Technology, especially with businesses dealing with vast amounts customer information, cyber threats are tremendously on the rise. Cyber liability insurance reduces the financial risk of a data breach so that businesses can accommodate the related costs and work on restoring its customer’s trust.

Understanding Cyber Liability Insurance:

It is therefore imperative to have cyber risk management in the modern world economy most especially so for the companies that engage in acceptance and processing of electronic payments. This one covers the financial risk that may be incurred in the occurrence of the cybercrimes, hack attacks, and all other related risks.

Key Components of Cyber Liability Insurance

- Data Breach Response Coverage: Pays for giving notice to the individuals who have been affected, to give public notice, to have their credit report monitored, for attorney charges, and for investigative charges.

- Cyber Extortion Coverage: Offers protection against monetary loss due to ransomware attacks or any other brand of cyber extortion other than hacking crimes.

- Business Interruption Coverage: Aids to cover up for loss of income in the event that a cyber risk affects business in the long run, in terms of slowing down or halting business.

Media Liability Coverage: Corrals with protection from actions of defamation or libel, or cases of infringement of copyright as caused by the use of the internet. - Cyber Crime Coverage: To cover losses associated with direct attacks on wire transfer and phishes, as well as other cyber threats.

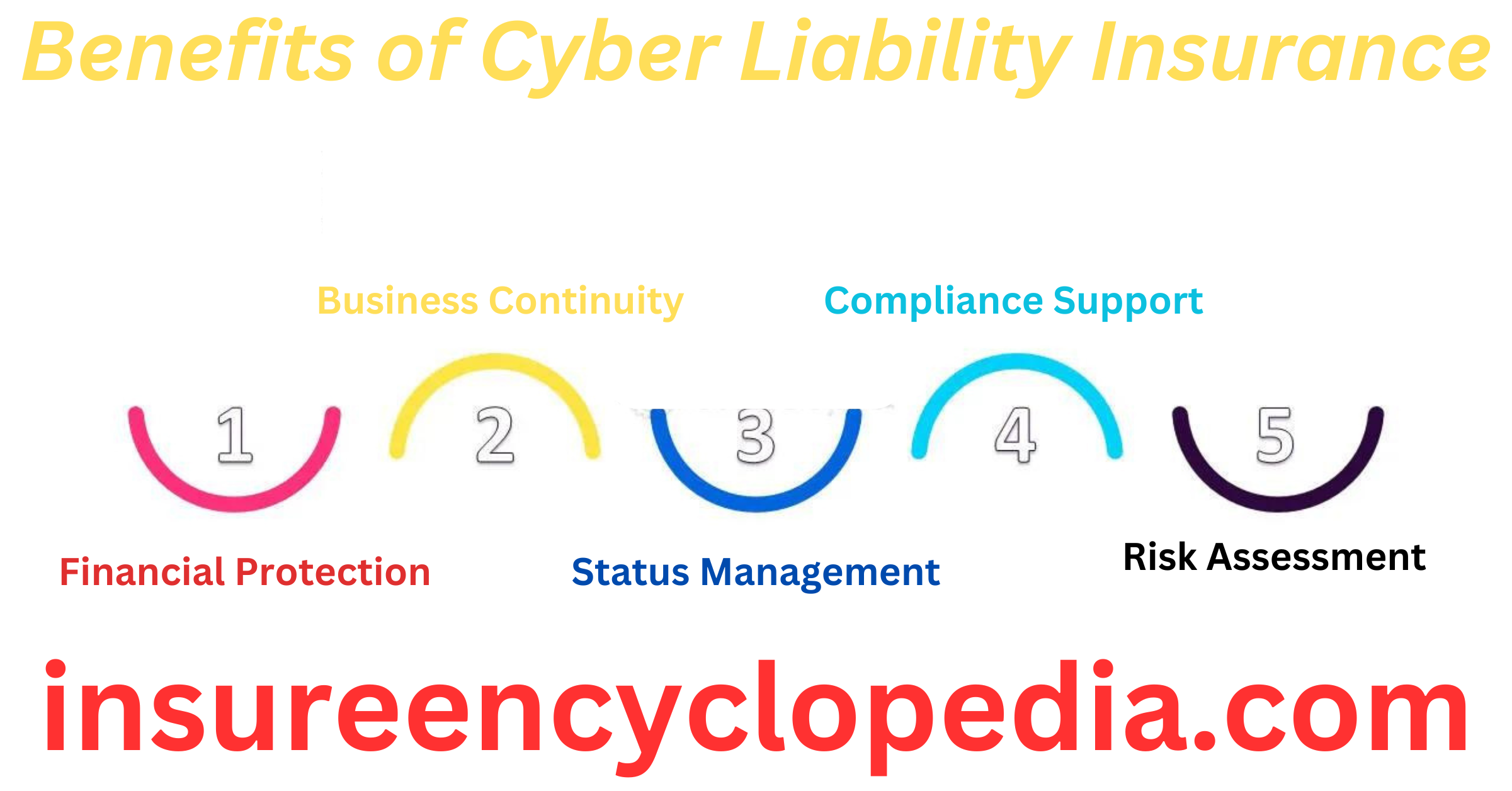

Benefits of Cyber Liability Insurance:

- Financial Protection: These are costs like legal costs, fines given by the regulators and public relation costs in the instance of a data breach.

- Business Continuity: Can help maintain the organization through the disruption caused by the cyber-attack through covering for business interruption risks.

- Status Management: Assists in the reconstruction of the reputation of your business after an incidence such as a data breach.

- Compliance Support: Provides links that help your business to meet the legal requirements on the legislation that relates to the running of corporations.

- Risk Assessment: The first step is to carry out a risk analysis so as to establish whether there are risks that exist.

Key Considerations:

- Policy Limits: It is wiser to define the right limits of insurance with the participation of a consultant under the consideration of the size of business and a risk level.

- Deductibles: Before enrolling understand how much of the direct costs you are ready to incur at the time of a claim.

- Exclusions: This will also help to avoid a situation whereby one engages in an activity that will not be protected by the policy.

- Policy Reviews: It is advisable to do it time to time to see whether it meets need of the business in the organization or not.

But in this regard, cyber liability insurance can turn into a powerful weapon, as long as one knows all the nuances of employing it.

Budgeting for Cyber Liability Insurance:

Indeed, cyber liability insurance is critical, yet it is an expense that can be quite heavy for organizations. Here are some tips on budgeting for this crucial coverage.

1. Understanding the Costs

- Policy Limits: Higher limits usually mean that the premium for it will be higher.

- Deductibles: Lower premium rate is associated with a higher deductible as this means that you have to pay more from your pocket.

- Coverage Options: Another factor is the optional such as cyber extortion or media liability that will affect the cost.

- Cost-Saving Strategies

- Risk Assessment: They use statistical analysis to determine likely claims and to this end they look for ways of avoiding or insuring against likely cyber threats in a bid to reduce premiums.

- Employee Training: Use professional training programs to reduce human’s mistakes in the system.

- Data Protection Measures: This requires practice of good data protection measures in handling patients’ data.

- Shop Around: Check quotes of the policies provided by different insurance companies.

- Bundle Policies: It may also be highly efficient to approach cyber insurance risks as a bundle of other business risks insurance.

- Review Coverage Regularly: It means that they should scale the coverage according to its changes for not overpaying for some facilities.

- Balancing Cost and Coverage

But the challenge of scouting for an insurance provider is to look for an insurance provider, which offers the best value for its cost while ensuring comprehensive coverage. Lack of proper insurance means that your business might be at risk, at the same time, over- insurance means that you would end up spending a lot of money on something that you do not need. Consult a selected insurance agent to identify the individual needs and come up with the right economic model.

Claiming Cyber Liability Insurance:

It is however useful to know how it is done despite the fact that filing such a claim may not be very easy. Here’s a general overview.

- Immediate Action: Notification can be given only when one realizes they are among the victims of the cyber-attack, and at this time, manage the situation, minimize the losses.

- Documentation: All reporting forms, loss reports, daily/weekly communication Logs and all other related working papers that you are using should be brought.

- Claim Filing: It should be ensured that all the parts of the insurance claim form of the company should be seen to be filled in which comprises of the description of the incident, the losses that have been incurred and the documents which you are attaching with the form.

- Investigation: The claim is then to be taken by the insurance company while in the process, more professionals on the other side may be included.

- Coverage Evaluation: Insurer will take necessary measures in relation to the disputed case against the terms and conditions of the policy with aim to decide whether or not they will implement the said provision.

- Claim Settlement: If it is so, the insurer pays out amount for actual losses being those which are regarded as being to the extent of the claim.